Research Briefing: How Whole Foods’ decisions impact CPG-retailer partnerships

In this edition of the weekly briefing, we examine Whole Food’s new mini stores and its impact on emerging CPG brands as seen in data from Modern Retail+ Research.

Interested in sharing your perspectives on the future of retail, technology and marketing?

Apply to join the Modern Retail research panel.

Whole Food’s new store format shakes up CPG distribution

Breaking News: Amazon has announced that Whole Foods will be opening five downsized stores in NYC called “Whole Foods Market Daily Shop.” These smaller-scale stores are meant to speed up the customer shopping experience by downsizing to fewer product choices. The stores will focus on prepared foods, fresh produce and the company’s own brand, Whole Foods 365. As the concept continues to grow, new changes are likely to come to how other brands are distributed.

Questions: How will the new store format impact smaller CPG brands? Will emerging CPG brands still look to Whole Foods as a main retailer?

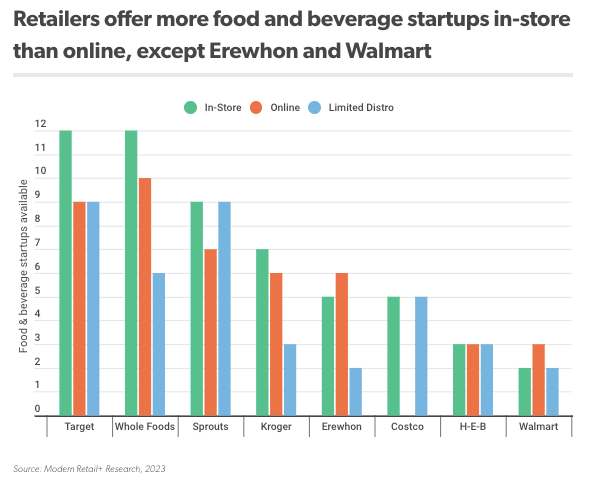

Answers From Research:

Whole Foods offers more emerging food and beverage brands than many other retailers, carrying 12 of the 14 food and beverage startups included in Modern Retail’s CPG distribution report. Whole Foods has committed to distributing over half (12) of the emerging brands that were considered in the study throughout its stores nationwide, with only six brands limited to certain regions of the U.S. Ten of the 12 brands Whole Foods carries in stores can also be ordered on the company’s website. Because Whole Foods is a subsidiary of Amazon, Whole Foods customers have access to a quick distribution and delivery powerhouse. According to Modern Retail’s analysis, Whole Foods’ ability to deliver online orders rapidly makes it an optimal choice for newer CPG brands that need a strong distribution partner.

As a major player in the premium grocery space, Whole Foods is a stand-out partner for specialty brands, according to Modern Retail+ Research, especially because startup brands are often priced higher than legacy brands in order to achieve higher margins. This becomes a challenge for those startups when they appear on shelves next to lower priced brands at more affordable grocery stores like Kroger and Sprouts. In premium grocery stores, however, startups sit among other premium brands in a similar price range. With less pricing competition on the shelf, a startup can focus on its branding and product differentiation to capture customers.

Want to learn more: Modern Retail+ Research’s analysis CPG distribution examines the direction that emerging CPG brands are headed for retailer partnerships.

READ MORE ABOUT CPG DISTRIBUTION

See research from all Digiday Media Brands: