Why legacy players like Mastercard & Citi are testing out the online checkout space

As venture capital for fintech start-ups stagnates, legacy financial institutions are continuing to integrate their services into the online checkout experience.

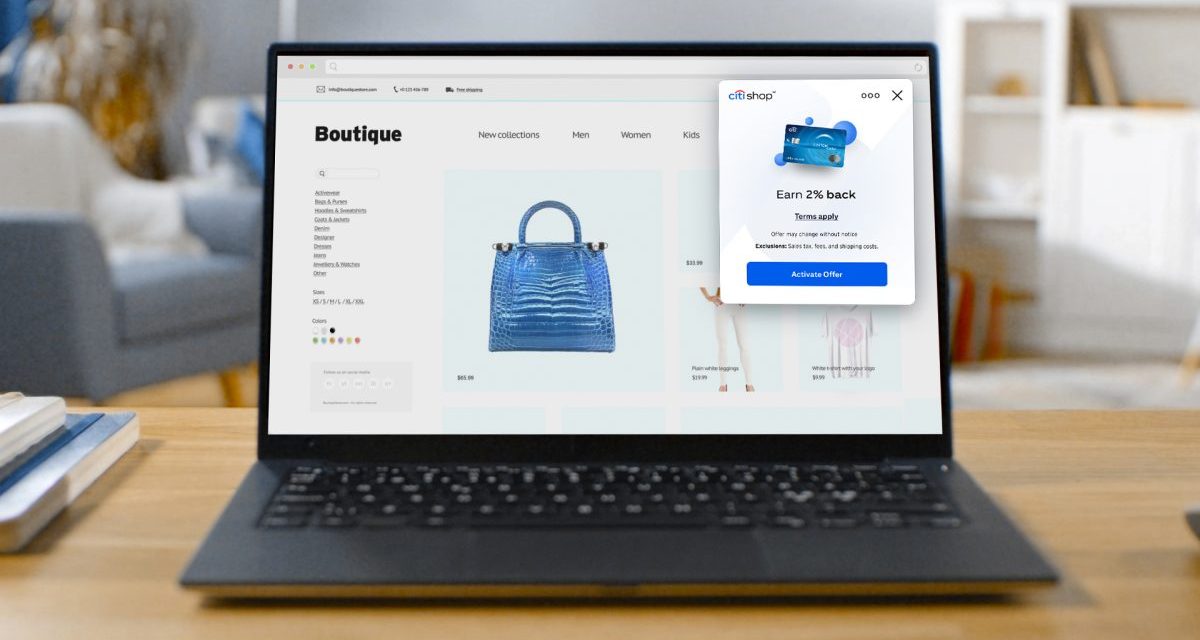

Last week, Mastercard announced a new biometrics service aimed at streamlining e-commerce logins and payments by using fingerprints or facial recognition to access customer accounts. It’s the latest addition to its growing suite of APIs and services for online merchants. Additionally, Citi unveiled Citi Shop, a browser extension that will reward customers with a statement credit for shopping at select online stores.

The advent of e-commerce led to a bevy of buzzy startups, with major players like Block and PayPal continuing to drive business. But smaller fintech players are beginning to experience a lull in funding. Pitchbook found the sector saw a 43% year-over-year decline in venture capital fundraising in 2023 compared to the year before. Factors like higher interest rates, rising costs of capital and slowdown in business growth drove down investment in the space.

But big financial institutions, buoyed by account services and other products, have room to experiment. In Mastercard’s case, it’s building the rails for a system that aims to make it easier to complete your transaction. Citi Shop, for its part, will reward existing customers for shopping at partner merchants. The network is launching with around 5,000 shops.

Staying relevant

Part of the reason it makes sense for banks to pursue checkout-based services is because they may carry a degree of trust with a shopper that a startup can’t command. Gallup in 2023 found that 26% of U.S. residents had “a great deal”or “quite a lot of trust’ in banks — more than said the same for Congress, news channels, “big business,” organized labor or the criminal justice system. And it may depend on the kind of bank; Morning Consult found last year that while less than half of people said they trusted digital banks, 69% trusted credit unions.

There are also generational shifts to consider. A Morning Consult survey in November found that while there is currently high trust in financial services, providers “must lean on digital innovation for growth” as Gen Z and millennials require more financial services.

Citi’s head of proprietary products Anthony Merola said Citi Shop is a response to explicit customer feedback for a rewards program. Shoppers want to save, he said, and Citi Shop provides a quick way to a get a deal. The statement credits will be a percent of the total amount spend, and attributed to the account in 60 to 180 days. The service also finds coupons.

Citi’s own research shows that while 74% of U.S. shoppers say they’ve abandoned their cart because they couldn’t find a promotion, 65% of them are more likely to use a browser extension if it’s created by a bank or a financial institution.

The browser extension world is riddled with couponing programs and money-saving apps, whether that’s code-based services like PayPal’s Honey or reward-driven ones like Rakuten. But Capital One Shopping, a service that the bank has operated going back to 2018, is the number one free lifestyle app in the Safari Extensions catalog. The extension looks for coupon codes to apply to an order and can help cardholders rack up rewards and statement credits.

While Citi wouldn’t share how many customers or transactions Citi Shop saw in its first week, Merola said existing customers will get notices that the program is live, and that the model could evolve or expand as times goes on. The U.S. personal banking division is a “bright spot” in the bank’s performance, CEO Jane Fraser said in a 2023 earnings release, with new accounts for Citi-branded cards seeing a 9% year-over-year increase.

“Feedback led to the launch of this, and it’ll be continued feedback that leads us to the evolution as well,” Merola said.

B-to-B opportunities

Yet it’s not just the customer-facing part of the checkout experience that will help give big banks a way to secure their role in an e-commerce future. Virtually all major banks already offer merchant services, while the credit card networks Visa and Mastercard play important roles in credit card processing systems. For Mastercard, the new biometric services can use a face or fingerprint for logging in customer accounts or loyalty programs, where someone can have their shipping and billing information stored.

“We’re a brand of trust,” said Dennis Gamiello, the executive vice president of identity products and innovation at Mastercard. “We have a role to play in setting the standards as well as delivering the solutions that enable the ecosystem to offer a more seamless and secure experience.”

The service aims to provide a smoother customer experience — no scrambling to remember passwords — while ensuring customer information is safely stored, Gamiello said. While Mastercard has previously rolled out biometric pilot programs, this system is the first business-to-business offering that will allow merchants to get a biometric login for their systems.

“The urgency is there now just to compete in the digital era to have the best experience. Biometrics is kind of a cornerstone to those strategies,” he said.

Put together, these new offerings show that the payments world is constantly in flux — and even legacy players are trying to get in on more parts of the business. Bryce Deeney, the founder of Equipifi, which works with banks and credit unions to create buy now, pay later-style installment payment plans, said that his “a-ha” moment in creating the company stemmed from the need for legacy financial institutions to compete for “top of wallet status.”

“Banks are brands too, just like Affirm and PayPal, and they have to defend their brand to stay relevant,” he said.