BNPL usage surged during Q1 as middle-income shoppers increased adoption

Buy-now, pay-later services are booming as low- to middle-income consumers look to stretch their budgets.

Earnings results from both Klarna and Affirm this month showed significant growth in gross merchandise volume (GMV) on their platforms, as well as upticks in overall users. Klarna reported last week that its GMV hit $33.7 billion, a 33% year-over-year increase, and Affirm’s GMV for its most recent quarter hit $11.6 billion, a 35% year-over-year increase and the 10th straight quarter of over 30% growth. Meanwhile, new reports indicate that BNPL usage among middle-income households, specifically, has picked up.

The services are also seeing that shoppers are hungry not just for splitting up payments over time, but also for special deals. Last week, Affirm held “The Big Nothing” three-day sales event that offered 0% interest across thousands of brands. The campaign outperformed the inaugural edition in October with about 35% more sales. Average cart sizes were $712, up 50% from October. The 0% APR offers are funded by the merchant, and Affirm says it saw a 70% uptick in the number of offers this time around.

“Our Big Nothing works because the whole network shows up at once — real 0% APR offers from merchants, real demand from consumers,” Vishal Kapoor, Affirm’s svp of product, said in an email.

For brands, the BNPL surge indicates that the spending tools are becoming a way to attract shoppers looking to finance purchases outside of traditional credit channels. New data from Consumer Edge shows that about 20% of BNPL users used three or more different services for such purchases, up from 12% five years ago.

The platforms themselves are looking to get in front of more customers for in-store purchases by pushing physical cards that let users split purchases, as well as by continuing to show up at new merchants’ online checkouts.

Max Levchin, CEO at Affirm, spoke on the most recent earnings call about how the company continues to gain share and why shoppers are getting more comfortable with the products. Beyond a 22% year-over-year increase in active users, the third-quarter data showed that 95% of transactions came from repeat customers.

“There are people who have decided Affirm is their jam, and that’s what they’re going to use,” he said, according to a transcript. “It’s really compelling.”

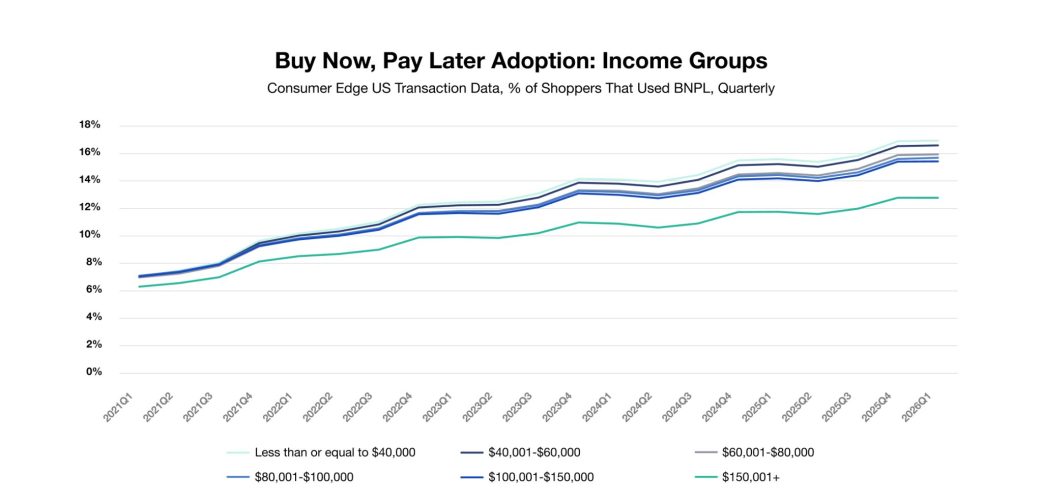

Widespread BNPL adoption across cohorts

A new report from Consumer Edge found that increased BNPL adoption is clustered among income groups earning up to $150,000 a year. While adoption is still highest among low-income households earning $40,000 or less, growth is just as prevalent among middle-income households earning $40,000-$150,000 a year.

Michael Gunther, svp of research and market intelligence at Consumer Edge, said the services are growing as lower- to middle-income groups feel increased financial stress. “They’re becoming more widespread as tools to help manage spending,” he said, similar to the growth in off-price stores, dollar stores and resale.

BNPL usage is also more common in households with children, at 18.7% penetration, compared to 12.4% for those without. The fast-growing demographic is 35- to 44-year-olds. Put together, the data suggest that BNPL is especially resonating with adults in the peak spending years of growing their households.

Gunther said another sign of the industry’s maturation is that people are using more BNPL services at once; the share of users with three or more services has nearly doubled since 2021.

At the same time, the financial stress hasn’t prevented people from buying.

“Not every [sector] has held up as well as others, but overall, we’ve seen consumer spending has held up remarkably well,” he said.

An increase in debt-fueled spending

While increased BNPL usage is good news for Klarna, Affirm and their shareholders, it also signals a further increase in debt-fueled spending. Credit card debt, for its part, has gone up. The latest data from TransUnion shows the average credit card balance was $6,715 as of the fourth quarter of 2025, up from $6,580 a year prior. Delinquencies of at least 30 days past due also increased across cards, auto loans, personal loans and mortgages.

Jessica Ramirez, co-founder and managing director of the consumer insights and advisory firm The Consumer Collective, recently released a 300-person survey on consumer spending called The Squeeze Report. It showed nearly 6 in 10 shoppers are dipping into savings to cover expenses. That was also true for about two-thirds of middle-income households.

Ramirez said the concern with BNPL is that it’s still a new debt stream for strapped consumers. She said it came up in fourth-quarter consumer interviews and surveys as a way that shoppers were financing the holiday season, and the stickiness has remained. Overall, nearly half of those surveyed said their debt has increased in the past six months, and 26% of them said they’re feeling overwhelmed.

“I’m cautious about what it means for the consumer side, but it makes sense that these companies are growing,” she said. “And I wonder if the economic situation doesn’t change, what it means for their growth and their business health moving forward.”

But BNPL services, which perform their own underwriting, point to the security of their underwriting systems to prevent them from issuing loans to people who may be credit risks. Affirm, which shares delinquencies for 30 days or more past due for its 0% and interest-bearing loans, shows that delinquency rates are hovering at around 2.8% for fiscal year 2026.

Klarna CFO Niclas Neglen said on last week’s earnings call that delinquency rates are tracking favorably, with both 30-plus- and 60-plus-day past-due rates declining quarter over quarter. “Our ability to continuously improve underwriting driven by transaction-level decisioning, short-duration exposure and the data set built on over $0.5 trillion of cumulative transactions since inception remains a key competitive advantage,” he said.