Exclusive: Affirm revamps its app to spur holiday spending

Fintech company Affirm today is announcing a mobile app redesign meant to incentivize more spending at its partner retailers this holiday season, the company told Modern Retail.

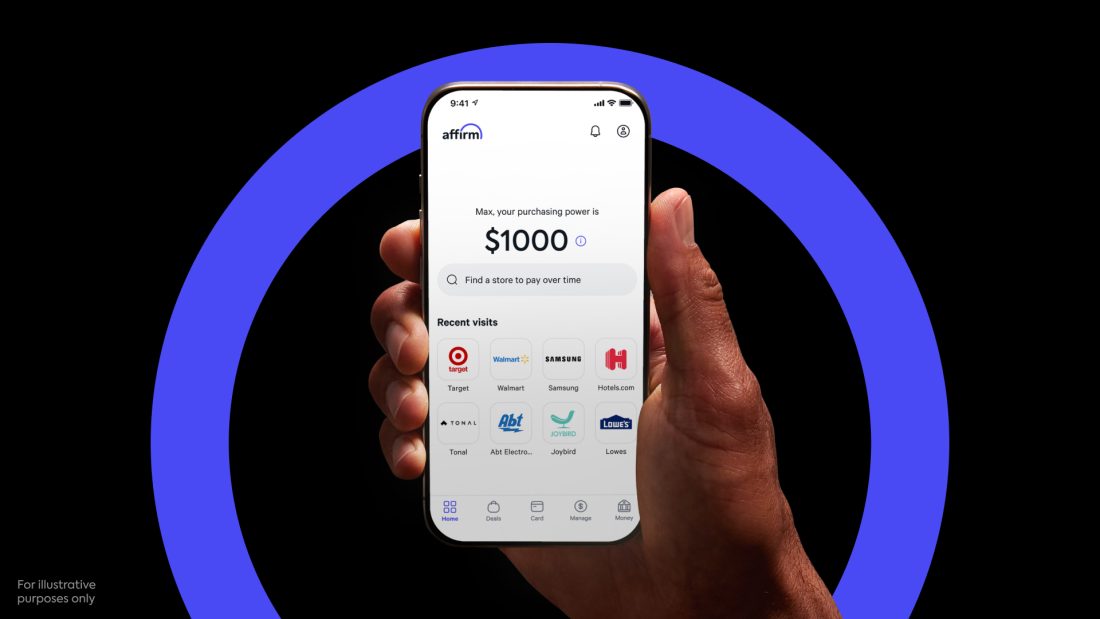

Affirm’s buy now, pay later offerings include pay-in-four loans as well as monthly installment plans up to 36 months, with either 0% APR or a fixed interest rate. Typically, customers have encountered these product options at the point of sale. Now, when users log into the newly redesigned app, the first thing they’ll see on the home page is their “purchasing power,” an estimate of how much they can spend overall using Affirm based on factors like their credit, income and where they shop. Vishal Kapoor, Affirm’s svp of product, said the payment network wanted to relaunch the app with new features that made it quicker and easier for people to see how much they could spend.

“The purchasing power feature existed before, but now we’ve brought it front and center. Customers really care about knowing how much they can responsibly spend with Affirm,” Kapoor told Modern Retail.

The timing of the rollout is meant to capitalize on holiday spending. Adobe predicts BNPL spending will hit $9.5 billion in November, the biggest month on record for the payment type. Cyber Monday is expected to bring in $993 million in spending alone, up from $940 million last year. “The holiday season is our Super Bowl, so we designed this app revamp to be ready for that peak,” Kapoor said.

Other updates include a new search function that allows people to see financing offers from Affirm’s partner retailers. These extend beyond the common interest-free pay-in-four model someone might see at checkout. Current advertised deals include a 6-month, 0% APR plan at Dyson and an 18-month finance deal with a fixed APR at Harley Davidson. Users can search by category — like home, shoes or fitness — or go directly to a retailer’s page. Affirm also counts retail heavyweights like Amazon and Walmart among its 300,000+ partners.

The app also allows Affirm users to see how much they owe on existing payment plans, as well as links to create an Affirm Money Account or Affirm Card.

The update is yet another sign that newer fintech players are upending the financing world with new products that appeal to younger shoppers. Affirm last month rolled out on Apple Pay. An Adobe report from February 2024 found that 8.8% of Gen Z respondents used Apple Pay within the past 30 days; just 4% of Millennial respondents, meanwhile, reported using the payment method.

This generation, in particular, is also showing an aversion to financing fees that BNPL may help them sidestep. An EY survey from January, for example, found that 69% of Gen Z shoppers use debit cards daily or weekly, compared to only 39% who said they frequently use credit cards.

The demand translates into significant growth for the companies behind the transactions. Affirm’s fourth-quarter earnings reporting in August cited $7.2 billion in gross merchandise volume, a 31% increase year-over-year. It reported revenue of $649 million, a 48% year-over-year increase. The company reported 24.7 million transactions in the fourth quarter, a 15% increase from the quarter prior and a 42% increase in transactions year-over-year. Yet Affirm still reported an operating loss of $73 million. Looking ahead, the company sees increasing consumer engagement and the number of transactions as its path to profitability, founder and CEO Max Levchin said in a shareholder letter.

With about 80% of Affirm’s 18.6 million active users downloading the app, the redesign is poised to encourage more spending. Kapoor said the company sees using the purchasing power number as a starting point for shopping. Then the customer can navigate the deals and offers within the app.

Ted Rossman, senior industry analyst at Bankrate, said BNPL tools are poised to grow this holiday season, in part because people are deal-conscious. Around one in four shoppers plan to spend more than 2023, according to Bankrate. Those who are watching their dollars may see an installment plan as “a kinder, gentler alternative” to putting a purchase on a credit card that could see interest rates as high as 30%. “It adds to up a frugal season where people are going to be conscious of their cash flow. BNPL fits right into that, enabling people to split things up into installments,” he said.

The downside, though, is that quick payments and alluring deals can make it too easy for some consumers to spend. NerdWallet reported earlier this year that about one in four Americans have used a BNPL product in the preceding 12 months. This has led to concerns about “phantom debt,” or owed money that’s not reflected on a credit report.

Like credit cards, Rossman said consumers have to be mindful about overspending with BNPL. “They can be like power tools,” he said of such products. “Really useful, or really dangerous, depending on how you use them.”

This critique is one that BNPL players like Affirm have heard time and time again. In response, most point out the relatively low delinquent rates. Affirm has said its delinquency rate is around 2.4% for payments that are 30 days or more past due and .7% for payments 90 days or more past due.

At Affirm, Kapoor said a shopper’s purchasing power — the number now shown on the app’s homepage — is assessed individually using machine learning models, statistical models and customer data. But that figure is not a guaranteed spending limit. Each individual decision is based on “hundreds of signals,” including a soft credit pull, income verification and the merchant the shopper is buying from.

Levchin said during the company’s last earnings call in late August that part of what has made the company successful at landing partnerships is its technological prowess. “Underwriting is hard. You got to get data. You got to get it in real-time. You have to verify it for both validity and accuracy and timeliness and all that good stuff,” he said. “It’s a real complicated thing that we do here really well. We’ve been at it for 13, 14 years almost now. That’s our DNA.”